What Affects Credit Score Most: A Simple Guide

If you're wondering what affects your credit score most, it really boils down to two main things: your payment history and how much of your available credit you're using.

While a few different elements go into calculating your score, these two are the heavyweights. They carry the most influence, making them the absolute best places to focus your energy when you're building or protecting your credit.

The 5 Factors That Shape Your Credit Score

Your credit score might seem like some mysterious number, but it’s really just a summary of five key pieces of information in your credit report. Think of it like a recipe—each ingredient matters, but some have a much bigger impact on the final taste.

Getting a handle on these components is the first step to really taking control of your financial future.

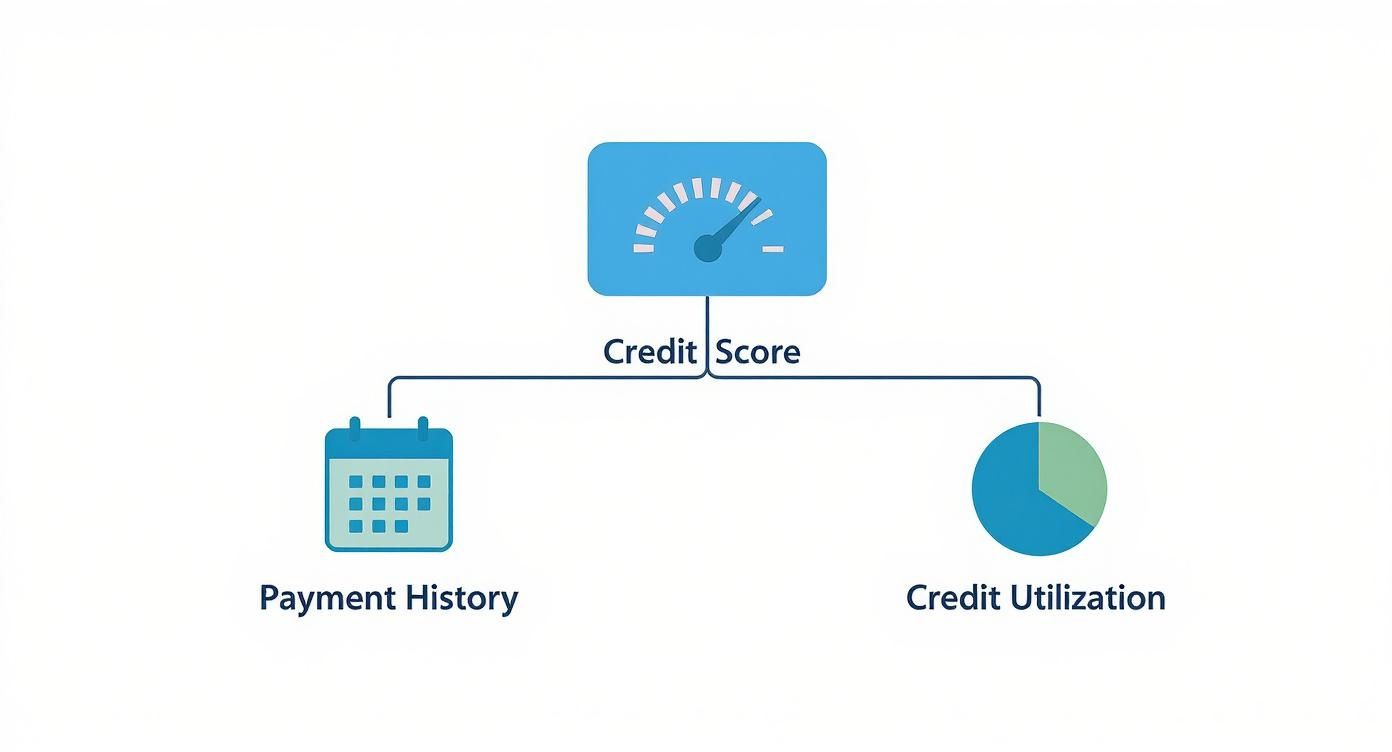

This visual gives a great breakdown of what goes into your score and shows just how important those top two factors are.

As you can see, your payment history and credit utilization together make up a massive 65% of your score in most scoring models. That means if you can get these two things right, you’re already well on your way to a great score.

If you'd like to back up a bit and cover the fundamentals first, our guide on what a credit score is is a great place to start.

Let's quickly summarize all five factors.

Credit Score Factors and Their Impact

This table gives you a clear snapshot of the components that make up your credit score and shows you where to focus your attention for the best results.

The takeaway is simple: consistently paying your bills on time and keeping your credit card balances low gives you the biggest bang for your buck when it comes to improving your credit.

Now, let's dig a little deeper into each of these five factors, starting with the most important one of all: your payment history.

Why Payment History Is Your Score's Foundation

If you think of your credit score as a building, your payment history is the concrete foundation holding everything up. It's not just another piece of the puzzle; it’s the single most important factor because it answers the one question every lender has: "Can I trust this person to pay me back on time?"

This isn’t just a nice idea—it’s baked into the math of how credit scores work. Your track record of paying bills on time is the best clue lenders have about how you'll handle money in the future. A long history of on-time payments shows you're responsible and reliable, making you the kind of person they want to lend to.

The Real Impact of a Single Late Payment

It's shockingly easy to underestimate how much one little mistake can hurt. A single payment reported as 30 days late can send a crack right through that solid foundation you've been building.

How big a crack? Well, payment history accounts for a massive 35% of your entire credit score. For someone with a pretty good score, just one late payment can cause it to plummet by 60 to 110 points.

And the damage gets worse the longer you wait:

If you want to get into the nitty-gritty of this, we have a complete guide on what a payment history is and how it all gets reported.

Building a Rock-Solid Payment History

The good news is that creating a strong payment history is actually pretty simple, even if you're just starting out with an ITIN. It all comes down to consistency and building smart habits.

To keep your foundation solid, try these simple strategies. First, set up automatic payments for at least the minimum amount due on all your accounts. Think of it as a safety net that guarantees you'll never accidentally miss a due date.

You can also set up calendar alerts or use a budgeting app to ping you a few days before a bill is due. This gives you plenty of time to make sure the money is there and pay it manually if you don't like autopay. If a bill does slip through the cracks and ends up in collections, it's crucial to know what to do next. Learning about disputing collections accounts can be a lifesaver in those situations. At the end of the day, a perfect payment history is your most powerful tool for building great credit.

Mastering Your Credit Utilization Ratio

Right after your payment history, the next biggest piece of the credit score puzzle is your credit utilization ratio (CUR). It sounds technical, but it’s really just a simple percentage that shows how much of your available credit you’re using at any given time.

Think of it like the gas gauge in your car. Your total credit limit across all your cards is the full tank. Lenders start to get a little worried when they see that gauge hovering near empty all the time. A high CUR can signal that you're relying heavily on credit to get by, which looks risky from their perspective. This one number says a lot about your financial habits and is a huge part of what affects your credit score most.

The Famous 30 Percent Rule

You’ve probably heard people talk about the "30% rule." It's a well-known guideline that suggests you should always try to keep your credit card balances below 30% of your total credit limit. So, if all your credit cards combined give you a 10,000 limit, you’d want to keep your total balance under 3,000.

This is a fantastic rule of thumb to live by, especially for ITIN holders who are carefully building their credit profile. Staying under that 30% threshold helps you avoid a major red flag in the eyes of the credit scoring models.

But here's a pro tip: 30% isn't a magic number. While staying below it is good, getting your ratio even lower is so much better. The folks with the very best credit scores? They often keep their utilization below 10%.

Practical Ways to Lower Your Utilization

The great thing about credit utilization is that you have a ton of control over it, and changes you make can boost your score relatively quickly. It just takes a little bit of hands-on management.

Here are a few simple but powerful strategies:

Not sure where you stand? You can find your exact ratio across all your accounts pretty easily. Our simple credit utilization ratio calculator can give you a quick snapshot.

Keeping this ratio in check is more important than ever. Nationwide, total credit card balances are projected to hit a staggering $1.1 trillion, meaning more people are carrying debt month-to-month. By keeping your personal utilization low, you immediately stand out from the crowd as a more responsible borrower.

How Credit Age and New Inquiries Affect Your Score

While paying bills on time and keeping balances low are the heavy hitters, two other factors play a huge role in your credit health: the length of your credit history and how often you apply for new credit. Together, these two pieces of the puzzle make up about 25% of your score—definitely enough to swing the needle one way or the other.

Think of your credit history like a financial track record. A long history with a solid pattern of on-time payments shows lenders you’re experienced and reliable. It proves you can handle credit responsibly over the long haul.

On the flip side, a flurry of applications for new credit cards or loans in a short period can make you look risky, as if you're suddenly desperate for cash. These two factors work in tandem to tell a story about your financial stability.

Why Your Credit Age Matters

This one is pretty straightforward—it's all about how long you've had credit. Scoring models like FICO and VantageScore want to see a proven history, so they look at a few key metrics:

A longer average age is always a good thing. It’s why you’ll often hear experts advise against closing your oldest credit card, especially if it doesn’t have an annual fee. Shutting down that account can erase years of positive history and cause your average age to drop, which can ding your score.

If you’re building credit with an ITIN, you might be starting from scratch. That's okay! The most important thing is to get started and be patient. Your credit age will naturally increase over time as you keep your accounts open and in good standing.

Understanding New Credit Inquiries

Whenever you apply for a credit card, mortgage, or auto loan, the lender pulls your credit report. This is called a hard inquiry, and it can cause a small, temporary dip in your score. Having one or two hard inquiries over the course of a year is totally normal and won’t hurt you.

The problem arises when you have a bunch of hard inquiries in a short amount of time. To a lender, this can signal that you're in financial trouble and are scrambling to open new lines of credit, making you a higher risk.

It's also crucial to know the difference between a hard inquiry and a soft inquiry. Soft inquiries happen when you check your own credit or when a company pre-qualifies you for an offer. These have zero impact on your credit score.

There’s a smart exception to the hard inquiry rule, though: rate shopping. Credit scoring models are designed to know that when you're looking for a big loan, you're going to compare offers. Any inquiries for the same type of loan (like a mortgage or auto loan) made within a 14 to 45-day window are typically bundled together and treated as a single inquiry. This lets you find the best deal without wrecking your score.

Your Credit Mix and the Bigger Economic Picture

While it’s not a huge piece of the puzzle, your credit mix does matter. It accounts for about 10% of your score, so it's worth understanding. Lenders want to see that you can juggle different kinds of debt successfully. It’s a bit like a job resume—having diverse experience makes you look like a more capable, well-rounded candidate.

A strong credit mix usually has a bit of both of these:

Having both types shows financial discipline. But here’s a crucial piece of advice: don't ever open a new account just to "improve your mix." The small boost you might get isn't worth the hard inquiry on your report and the risk of taking on debt you don't actually need. A good mix tends to happen naturally over time as you go through life.

How the Economy Can Sway Your Score

Your credit score doesn't live in a bubble. The economy itself can create headwinds that make it harder to manage your debt, which is a core part of what affects your credit score most. While your own financial habits are firmly in your control, it helps to be aware of how outside forces can throw a wrench in the works.

When the economy takes a turn, it can ripple through every part of your financial life, from your job security to your weekly grocery bill. High inflation, for example, stretches your budget thin, which might lead you to lean more heavily on credit cards and carry higher balances than you'd like.

Broader trends like inflation and interest rates can indirectly put serious pressure on credit scores. When inflation rates creep above 5%, as they have in recent years, it eats into your purchasing power, especially for families on a tight budget. This can increase reliance on credit just to make ends meet.

At the same time, rising interest rates often cause banks to tighten their lending standards. This makes it tougher to get approved for new credit or even keep the credit lines you already have. For a deeper dive into these patterns, you can check out a recent report on global credit trends.

This is exactly why building a solid financial foundation is so critical. If you make it a habit to keep your credit card balances low and always pay your bills on time, you create a financial cushion. This buffer helps protect your score when the economic weather gets rough, safeguarding all the hard work you’ve put into building a positive credit history.

Common Questions About Your Credit Score

Diving into the world of credit can feel like learning a new language, and it's easy to get tangled up in myths and half-truths. Let's tackle some of the most common questions head-on, especially for those navigating the U.S. financial system for the first time.

Getting clear, straightforward answers is the first step. It helps you focus on what actually works for building a solid financial foundation.

Does Checking My Own Credit Score Lower It?

This is one of the biggest myths out there, and the answer is a firm no. When you check your own score—whether it's through a credit monitoring service or your bank's app—it's what's known as a soft inquiry. Think of it like looking in a mirror; it doesn’t change your reflection. You can, and absolutely should, check your score as often as you want to see how you're doing.

A hard inquiry is different. That’s when a lender pulls your credit report because you've officially applied for something, like a new credit card or a car loan. This can cause a small, temporary dip in your score, but it's usually less than five points.

How Long Do Negative Items Stay on My Report?

Most negative marks, like a late payment or an account that went to collections, will stick around on your credit report for seven years. Something more serious, like a Chapter 7 bankruptcy, can stay on your record for up to ten years.

But here’s the key thing to remember: the sting of these negative items fades over time. A late payment from six years ago has way less impact on your score than one from last month, especially if you've been piling up positive payment history since then.

Can I Build Credit With an ITIN?

Yes, you absolutely can. This is a huge point of confusion for many newcomers, but you don't need a Social Security Number to build a credit history in the U.S. More and more banks and credit card issuers are now happy to accept applications from people using an Individual Taxpayer Identification Number (ITIN).

You can apply for specific ITIN-friendly credit cards or loans and start building your financial resume. The game plan for success is exactly the same for everyone:

Building a great credit history with an ITIN is completely within your reach. It's a powerful step toward feeling financially secure and included in the United States.

Take the guesswork out of building your financial future. itin score provides the tools you need to build, monitor, and understand your credit with an ITIN, all for free. Get your personalized credit-building plan today at https://www.itinscore.com.